Inside Software 05.03.26: What does it really take to get to $1B?

Every week we’ll provide updates on the latest value levers and trends operators are asking us about in Technology and Software. If there are things you want to hear more about - shoot us a note.

With all the AI excitement, there’s a foundational question worth asking: What does it actually take to build a $1B software company? For a long time, $1B felt like a glass ceiling, reserved for a short list of giants. But over the last decade, that ceiling has been shattered… repeatedly. So we asked: What are the repeatable patterns behind the teams that got there the “hard way,” not the overnight category winners, but the companies that kept expanding their ceiling through deliberate execution. My colleagues Sushil Upadhyayula, Kenzie Haygood, and Greg Fiore did some exciting, data-driven research to provide visibility into “what it takes”

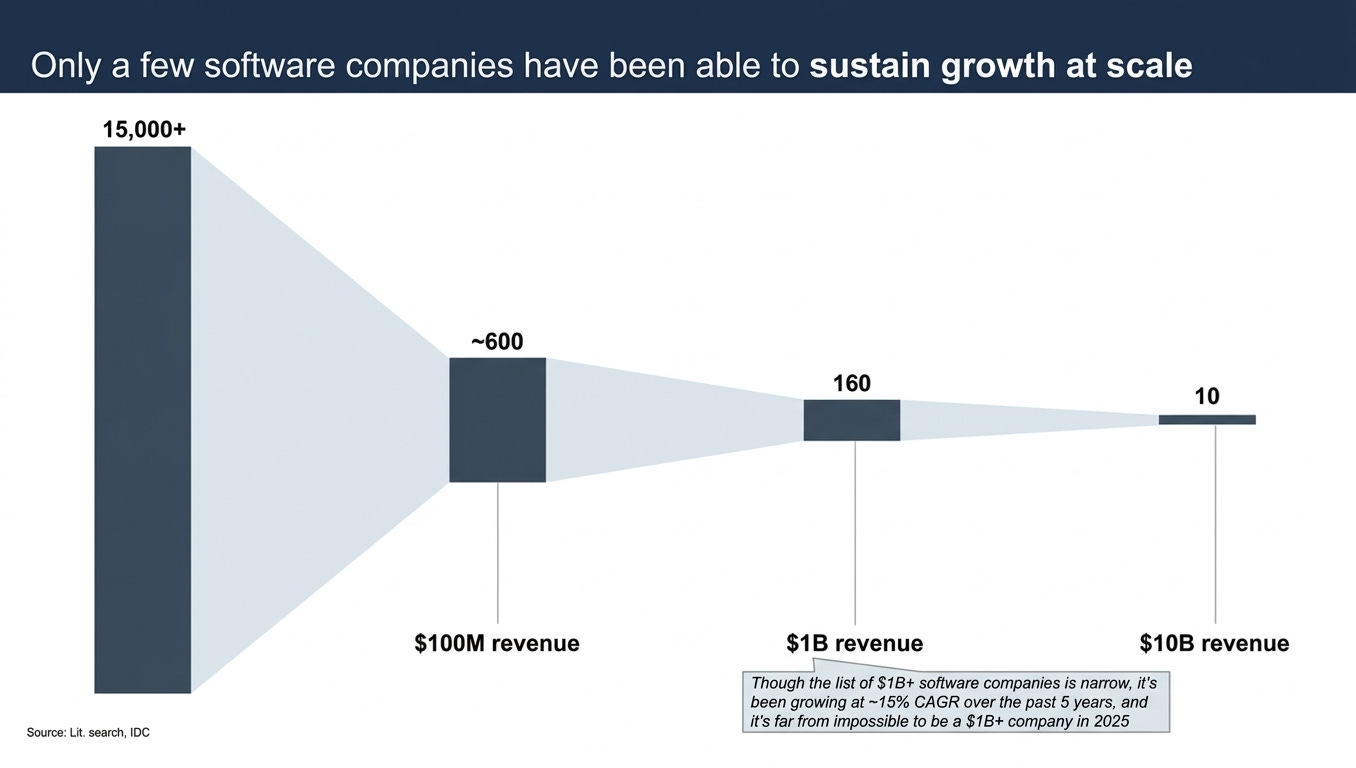

Here’s the first exciting stat: ~160 software companies have crossed $1B in annual revenue (out of roughly ~600 that have made it to $100M). The club is still selective, but it’s growing fast, and the ceiling is clearly breakable.

And it’s worth saying plainly: getting from $100M → $1B isn’t “slow,” it’s an unusually fast compounding engine. The “typical” journey is ~8 years, which implies sustaining ~30–35% growth through the law-of-large-numbers zone. That’s the point: you don’t drift into $1B. You earn it with a multi-year plan that stays ahead of your own deceleration.

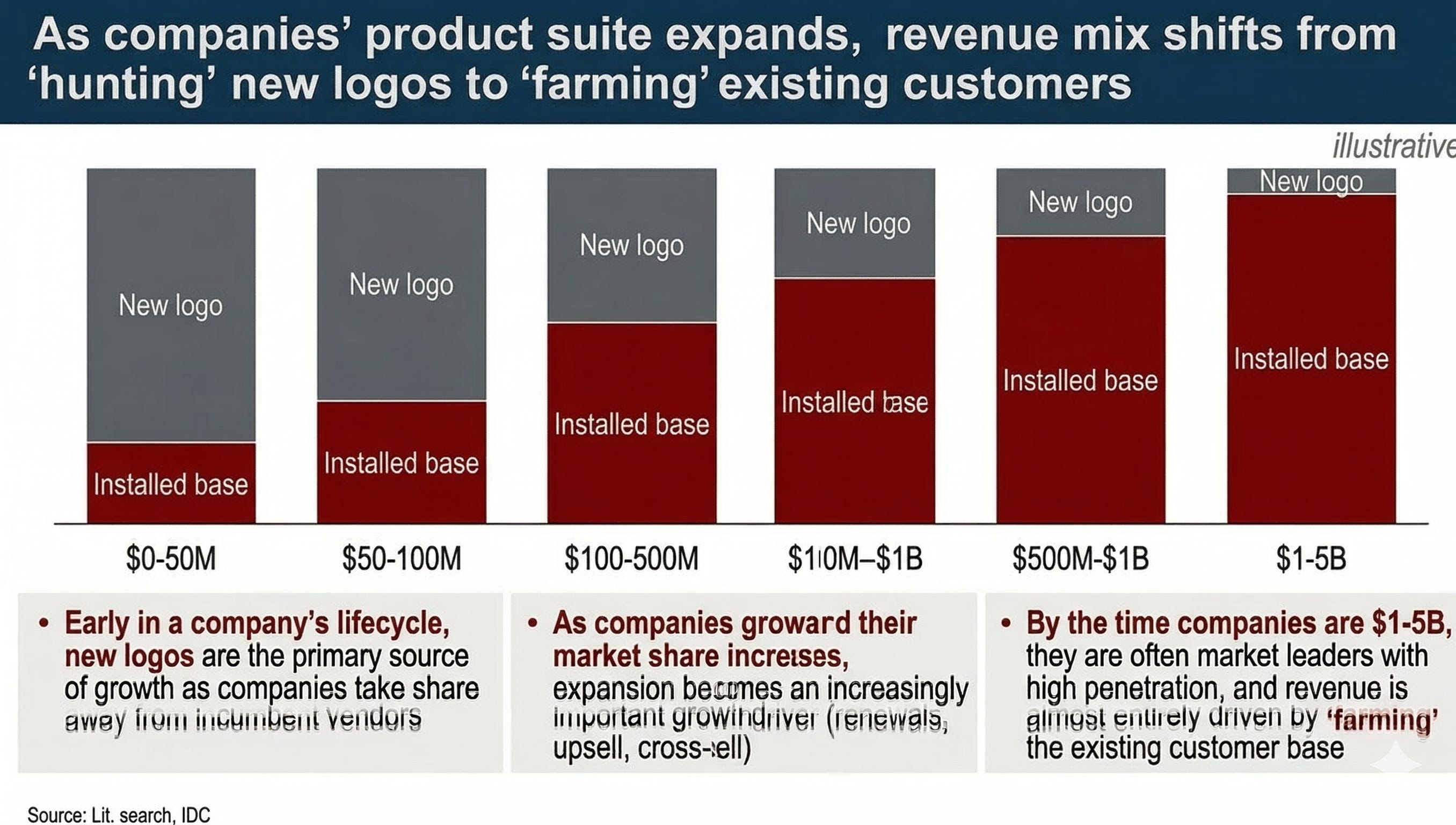

Now here’s the part teams forget (until it’s too late): as you scale, the growth mix flips. Early on, you’re “hunting” (new logos). Later, you’re “farming” (renewals + upsell + cross-sell). In the benchmark we reviewed, new logos drop from ~75% of growth at $0–50M to ~15% at $1–5B (and ~5% at $5B+), meaning your product portfolio and your GTM muscle have to evolve, or gravity wins.

So what separates the relentless TAM expanders? They don’t just optimize the core. They expand it across four vectors (usually more than one at a time):

New products / buying personas. By the time companies are $1–3B, ~80%+ sell 2+ major products. In the sample we tore down, the “typical” $1–3B portfolio looked like: ~17% still at 1 product, ~33% at 2–3 products, ~33% at 4–5 products, ~17% at 6+. Translation: single-product purity is awesome… until it caps your ceiling.

New geographies. This one is less optional than people admit. In the analysis of ~$1B+ software firms, >2/3 generate at least ~30% of revenue outside their primary region. Our cut of the data told a similar story, roughly ~3/4 were below 70% “home geo” concentration.

And here’s the gotcha we keep seeing in the wild: a surprising number of companies hit $500–700M with a footprint that’s essentially “English-speaking plus”(US/Canada/UK/Australia/NZ) then finally decide it’s time for Europe. Continental Europe is a step-change harder (localization, channel structure, procurement norms, regulatory nuance, and a very different density of reference customers). If you’re “just starting” international at $600M, plan for a couple of slower cycles while you build the muscle, because it’s not a switch you flip on the way to $1B.New segments (SMB → MM → Enterprise, or vice versa). This sounds obvious, and it’s also where good companies faceplant, because segment moves usually require a different product, different channels, and a different cost-to-serve model. One company example we’ve studied made the classic move up-market: it pushed into Enterprise, crossed $1B+, and ultimately drove 40%+ of revenue from Enterprise. Not even then, performance and unit economics looked very different from its mid-market core.

New verticals. Vertical SaaS winners don’t stay single-vertical forever. In the benchmark set (N=23), 0% stayed in only one vertical; about ~13% played in 2, ~35% in 3, ~35% in 4, and ~17% in 5+. Adjacent vertical expansion is often the difference between compounding… and topping out.

21")

What we want you to take away: $1B is rarely one TAM. It’s usually a sequence of TAMs, stacked over time. And the sequencing matters: you often need to place (and staff) the next bets 2–4 years before the core starts to saturate, because GTM rewiring + product scope expansion + capability building don’t happen in a quarter.

One last twist: these dynamics get even sharper in the age of AI. As AI features (and agents) get embedded into workflows, “farming” becomes the main event because the easiest path to durable growth is expanding value inside the installed base (more use cases, more personas, more attach). But that only works if you’ve done the hard work: packaging that makes sense, CS motions with real swim lanes, product that’s genuinely “better together,” and a roadmap that’s built future-back instead of “whatever we can ship next sprint.”

Call to action: if your plan still sounds like “keep selling harder,” this is not a wait-and-see moment. Start pressure-testing your path across products, geos, segments, and verticals…and be honest about which ones you need to start building now to avoid stalling later. And if you don’t know where to start… ask. Don’t burn two years “figuring it out” while the market keeps moving.

Note: The opinions expressed in this article are my own and do not represent the views or specific practices of Bain & Company. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.