Inside Software 05.31.26: Growth is back. In software, product is doing more of the work

Every other week we’ll provide updates on the latest value levers and trends operators are asking us about in Technology and Software. If there are things you want to hear more about - shoot us a note.

The setup: growth ambition is back, but execution is harder

A few weeks ago, we wrote that software is entering the “year of product.” Said differently: the old formula of “add more reps, get more growth” is losing some of its punch, and the next chapter will be defined more by how much value a product can create quickly, visibly, and repeatedly. My colleagues Jamie Cleghorn and Rob Stein recently released Bain’s B2B Growth Agenda 2026, a scaled longitudinal survey designed to capture the sentiment of growth leaders, makes that argument feel even more real. Across more than 1,100 commercial leaders, the message is not that companies are backing away from growth. It is almost the opposite. Leaders are entering 2026 with more ambition and plenty of confidence. But they are doing it in a market that feels faster, more volatile, and much harder to execute in than it did just a few years ago.

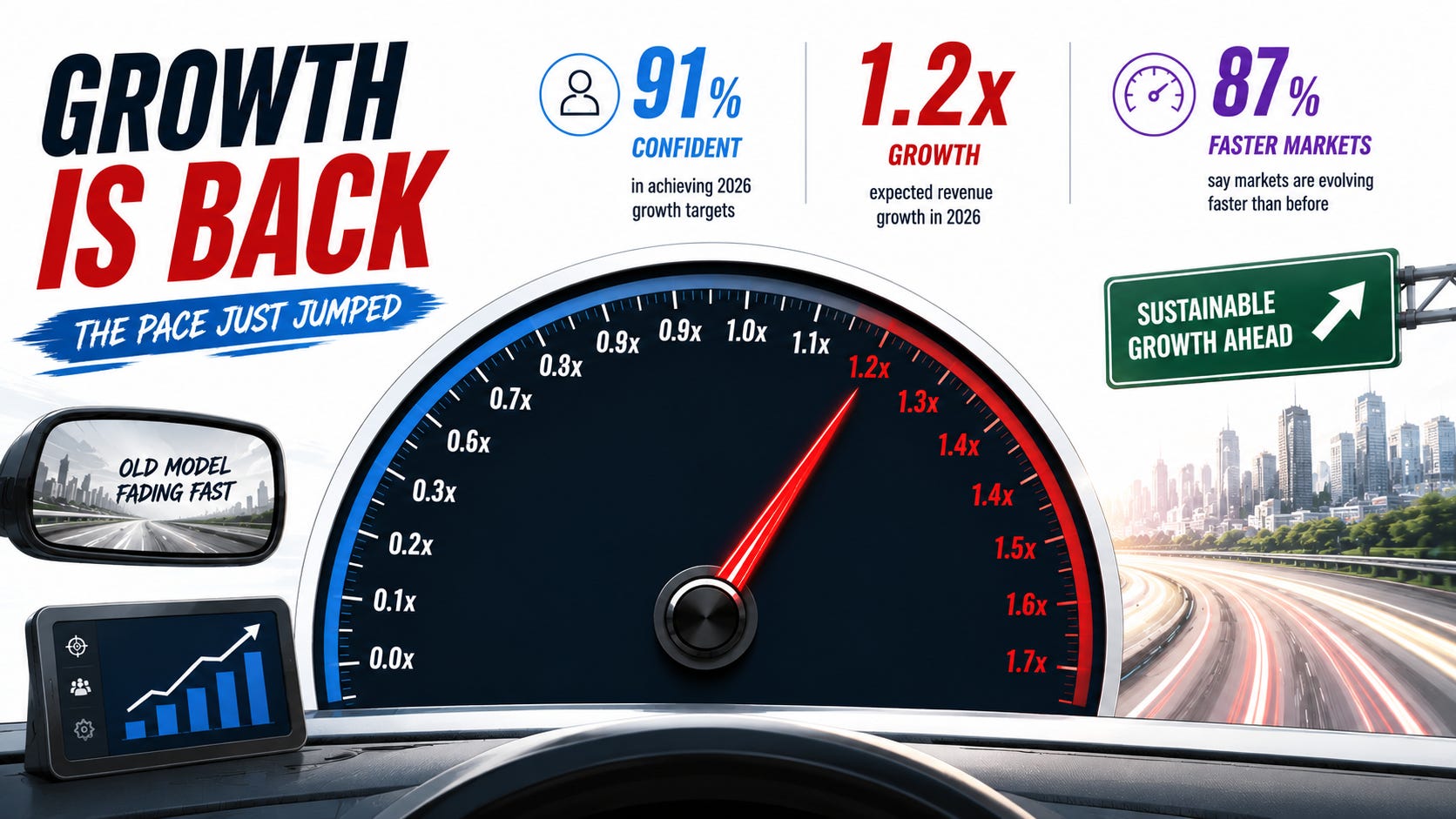

Start with the overall market. The broad mood is not defensive. It is aggressive, but uneasy. 87% of executives say their markets are evolving faster or significantly faster than before, driven primarily by AI and automation, geopolitical and regulatory shifts, and changing customer buying behavior. At the same time, more companies are missing their numbers. Roughly a third missed revenue targets in 2023; by 2025 that number had risen to about 42%. And yet confidence has not broken. Roughly 91% of leaders say they are confident in hitting 2026 targets, and expected 2026 growth rates are about 1.2x 2025 levels. That is a pretty remarkable combination: rising ambition, rising confidence, and worsening delivery. In our view, that is the setup for 2026 in one sentence.

The implication is that the market still wants growth. It just cannot brute-force its way there the way it once could. The top challenges executives cite for 2026 tell the story well: pricing pressure, market uncertainty, acquiring new customers, modernizing GTM technology, and using analytics and AI effectively. None of those are solved by simply adding more people. And the winners are showing that. Across sectors, the best performers are growing 1.6x faster than peers and converting that advantage into roughly 2.0x TSR over six years. How? Not with a magical new playbook. They are getting sharper on the fundamentals: a clearly activated value proposition, better customer targeting, more disciplined sales motions, and AI embedded into real ways of working. Even at the market level, this is already less a headcount story and more a leverage story.

Software is feeling the pressure more acutely

If that was the picture across the full market, Bain’s Inside Software team also pulled out the feedback specifically from software growth leaders. That feedback follows the same pattern, but with sharper edges and less room for error. Software market valuations are down ~15-25% year to date through late May. About 90% of software executives say their markets are evolving faster, with AI and automation, new market entrants, and shifts in buying behavior sitting right at the top of the list. The ambition is still there: software companies also expect 2026 growth rates to run about 1.2x above 2025. But the execution gap is harder to ignore. The share of software companies missing revenue targets rose from 24% in 2023 to 40% in 2025, even as roughly 80% head into 2026 confident they can hit the plan. So software is not in retreat. But it is operating in a much harsher proving ground, one where confidence is still abundant, but forgiveness is not.

Product is carrying more of the growth load

This is where the survey starts to connect directly back to the “year of product” thesis. The most important software finding is not simply that the market is hard. It is that product and value proposition are increasingly doing more of the growth work. In software, companies with a fully activated value proposition grow about 1.5x faster than peers. Even more striking, companies creating offerings for new customers or segments grow about 3.5x faster. That is the survey’s cleanest proof point that growth is shifting upstream. The edge is moving toward businesses that have something sharper to say, something more differentiated to sell, and something more compelling for the customer to buy. In that world, product is not just supporting growth. Product is increasingly setting the pace for it.

GTM is still the multiplier

That does not make GTM less important. It makes GTM more accountable. Once product carries more of the burden, commercial execution has to be much more precise. The software winners in the survey are more deliberate and data-driven in how they prioritize accounts, with structured, data-supported account models more common among winners than laggards. More broadly, organizations that execute four or more sales plays, grow up to 1.9x faster. And winners are about 1.6x more successful at scaling AI-driven pricing, using real-time context to capture deals and value more effectively. So yes, product is doing more of the selling, but the best software companies are pairing that with tighter segmentation, more repeatable sales plays, and better pricing discipline. Product may create the right to win. GTM still determines how much of that right gets monetized.

The shift from headcount to leverage

The other major theme is one we highlighted in February: the model is shifting from headcount to leverage. Across the broader market, more organizations are increasing spend on productivity levers than on headcount growth, with about a 19-point gap in favor of productivity. In software, the same pattern shows up at about a 16-point gap. Automation and AI are the top spending priorities, and that makes intuitive sense. After a long period where tech sales hiring surged, growth has slowed to less than 1% annually. The message is not that companies no longer care about sales capacity; it is that they are looking for a different kind of capacity. The best teams want reps covering more accounts, managers spending more time coaching, and commercial organizations getting more output from better workflows instead of just more bodies. That is a meaningful change in the software growth model.

AI separates execution, not intent

And of course, AI sits right in the middle of this. But the software results are pretty clear that experimentation alone is not enough. More than 90% of software companies report AI experimentation. That sounds impressive until you look at the dispersion in results. Winners realize about 1.7x higher cost efficiency and about 2.2x higher revenue growth from AI than laggards. Why? Not because they ran more pilots. Because they embedded AI into workflows, built the right data and technology foundations, and treated AI initiatives like products with real ownership. Most companies are still early on true end-to-end, agentic workflow automation, so the gap today is not between companies using AI and companies ignoring it. It is between companies creating workflow-level advantage and companies still stuck in demo mode.

The bottom line

So, stepping back, the survey does not say software has a completely different growth agenda from the rest of the market. It says software is simply further along the same curve, and feeling it more acutely. The broad market is telling us that growth is back, but brute force is not. Software is telling us what that actually looks like in practice. Product matters more. Value proposition matters more. Pricing matters more. Precision in GTM matters more. AI matters, but mostly when it is embedded deeply enough to change how work gets done. That feels like the clearest read-through from the data.

To us, it is pretty simple: sales reps are not disappearing, but they are losing their monopoly on growth. The next phase belongs to software companies whose products create clear time-to-value, whose value propositions are activated consistently across the funnel, and whose GTM and AI motions amplify that advantage instead of trying to compensate for its absence. In other words, the survey does not overturn the “year of product” thesis. It quantifies it.

Wants to read more? Check-out are most popular recent posts

Inside Software 10.26.25 - How leaders are actually pricing in AI

Inside Software 03.01.26 - Congrats, you’re a leader, and somehow, you’re still behind…

Inside Software 03.29.26: The Agentic Reset for Product + Engineering

Inside Software 04.12.26: You Aren’t Moving Fast Enough (Zendesk Case Study)

Inside Software 04.26.26: Rule of 55? Hogwash! The Rule of 40 in an AI world

Inside Software 05.03.26: What does it really take to get to $1B?

Inside Software 05.17.26: The $100B Opportunity Hiding in the Boring Stuff

Note: The opinions expressed in this article are my own and do not represent the views or specific practices of Bain & Company. The information provided is believed to be from reliable sources, but no liability is accepted for any inaccuracies.

Your research suggests that product, AI, pricing, and GTM excellence are becoming increasingly important growth levers. What I'm curious about is this: among organizations with access to largely the same capabilities, what are you seeing as the primary explanation for the widening performance gap? Is it better capabilities, or better systems for converting capabilities into outcomes?